Six months in: How are house prices faring?

Oct 2020Karen Millers

Categories

Location ReportsMedia releasesNational market updatesPersonal advisersPIPA AdviserPIPA Annual Investor Sentiment SurveysPIPA Member ProfilesPIPA video updatesPIPA webinarsPodcastsProperty advisersProperty newsLatest Articles

Warracknabeal home buyer finds home in filthy state after buying property online

Location Report – City of Geraldton

Which property cycle are we in?

Rent rises ease but crisis’ link to population density found to be tenuous

Jordan van den Berg: The ‘Robin Hood’ TikToker taking on Australian landlords

We’re six months into the COVID-19 pandemic, and so far Australian property markets have weathered the economic storm quite well.

The data shows that median property values are starting to slowly trend down, but we’re nowhere near experiencing the 10%, 20% or even 30% drops that some industry experts predicted.

But are those price falls still to come?

The most recent data suggests that, if we continue on the current course, Australian real estate prices are set to continue down a path of resilience.

The RPM Real Estate Group’s latest quarterly Residential Market Review suggests that government stimulus packages and grants, particularly the HomeBuilder incentive introduced in early June (which offered $25,000 to anyone buying a new home), may have thrown the property and construction industry a lifeline – and could be responsible for putting a floor under the market going forward.

“The way that people work will likely change significantly post-pandemic, and this will have an impact on less traditional property investment locations” Peter Koulizos, chairman, Property Investment Professionals of Australia

In Melbourne, more than 50% of the quarter’s 3,786 total lot sales across Greater Melbourne and Geelong occurred in June, of which 69% were titled or near-titled lots, demonstrating the grant’s effectiveness at bringing forward buyer demand for eligible lots.

The June figures topped out at 2,043 lots, reflecting the strongest monthly sales result since November 2017 and contrasting deeply with the 654 lot sales recorded in April – the weakest result since the market hit the bottom in April 2019.

“During April we felt the crunch of social distancing restrictions, with a stark shift in spending patterns and wide-felt uncertainty across the workforce. Understandably, land sales stalled and the rental and apartment markets were heavily impacted too,” says RPM chief executive Kevin Brown.

“We saw lot sales steadily climbing to pre-pandemic levels through May, demonstrating underlying buyer confidence in Victoria’s property market, before activity really started escalating from early June with demand shifting notably to titled or near-titled lots.”

Brown says HomeBuilder made a marked difference to sentiment, and he welcomed the recent blanket extension of the grant across Victoria by three months, meaning that applicants now have six months from the time of signing an eligible contract to commence construction. However, he warned that a sudden drop-off in activity loomed large without further government intervention and suggested that a minimum six-month extension of the grant’s current contract and build timelines would help even out demand through the remainder of 2020 and into 2021.

It’s a sentiment echoed by Denita Wawn, CEO of Master Builders Australia (MBA), who says a strong building and construction industry is essential to a strong economy, and vice versa.

“Potential for price falls and reduced investor activity, together with historically low interest rates and government support, are propelling first home buyers into action” Andrew Bartolo, general manager home loans, ME

“In the Australian economy there is no industry with a bigger economic multiplier effect than building and construction. There is also no larger provider of full-time jobs and there is no other industry with as many small businesses; that is why we are seeking stimulus measures across the entirety of the residential, commercial and civil construction sectors,” she explains.

MBA is calling for a 12-month extension of HomeBuilder, among other things, to drive sustainable demand for new housing over the next 18 months.

In the short term, new housing activity remains robust, and while it’s impossible to predict where property markets might go from here, we can take a look at how markets have performed historically to get an idea of where they may be headed.

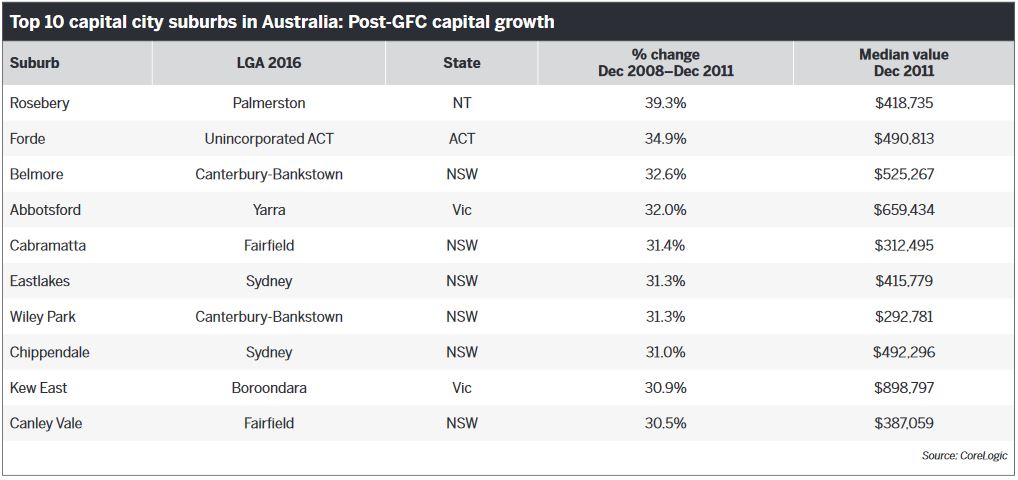

New research from Property Investment Professionals of Australia (PIPA) and CoreLogic, for instance, has identified the best-performing capital city and regional locations three years after the onset of the GFC.

The research and analysis, a joint initiative of PIPA and CoreLogic, found that capital city dwelling values increased by up to 39% over the three years from the end of December 2008.

This was just as government stimulus was ramping up, according to PIPA chairman Peter Koulizos, who says the capital city results showed a mix of inner- and outer-city suburbs, with six of the top performers being in Sydney (see boxout, p18).

Peter Koulizos, chairman, Property Investment Professionals of Australia

Peter Koulizos, chairman, Property Investment Professionals of Australia

“The dominance of Sydney in the results shows that nobody rings the bell to tell you when the upward swing of a property cycle has started,” he says.

“When you do hear it, it’s too late because it’s already begun. I say this because most people believed that property prices in Sydney only started firming a year or so later – in 2012 – when it was already underway but perhaps masked by the continued economic uncertainty around the globe.”

Across the country, Koulizos says the individual performance of each capital city was varied in terms of where the top-performing suburbs were located. In Melbourne, the best performers were inner-city areas, while in Adelaide it was homes located in outer suburbs that experienced stronger growth.

During the same period of time, the number of first home buyers also hit historic highs, because of the federal government’s First Home Owner Boost.

“The recovery in the property market was broad, varying from inner-city to outer-city suburbs, and certainly first home buyers helped by boosting demand for new properties, whether they were located in urban regeneration or greenfield sites,” Koulizos says.

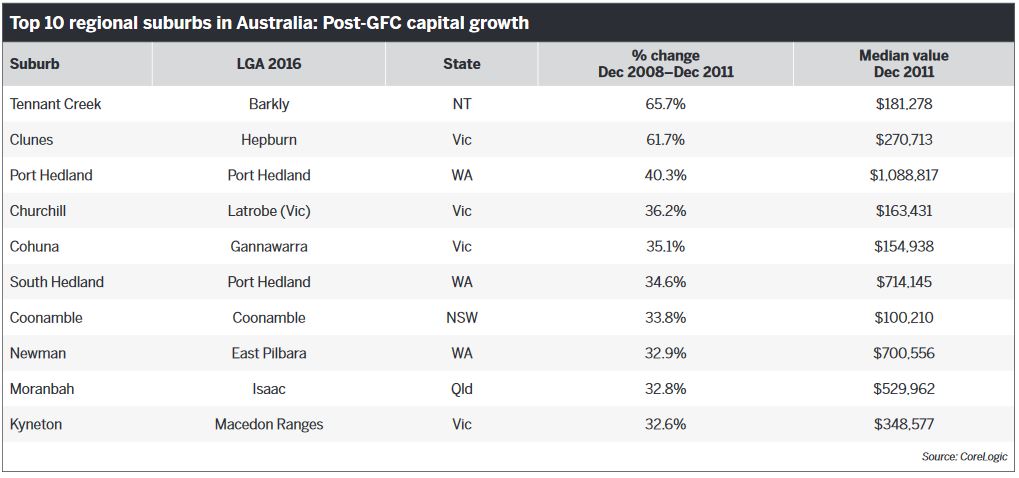

CoreLogic head of research Tim Lawless adds that dwelling values in regional areas increased by up to 65% over the period, with mining areas in particular performing well, given that the resources sector was firing on all cylinders at the time.

Tim Lawless, head of research, CoreLogic

Tim Lawless, head of research, CoreLogic

“Areas such as mining towns, where economic conditions are dependent on a single industry, are much more likely to experience bursts of price rises or falls because of the strength or weakness of their dominant industries,” he explains.

“While many of these mining regions recorded spectacular capital gains post-GFC, a few years later many of these same regions recorded a crash in home values.”

While the research shows the resilience of property prices during turbulent times, and Koulizos says prices are expected to stand firm over the medium term this time around, he cautions that the best-performing locations “may be very different to what has occurred in the past”.

“The way that people work will likely change significantly post-pandemic, and this will have an impact on less traditional property investment locations,” he says.

“Areas such as mining towns, where economic conditions are dependent on a single industry, are much more likely to experience bursts of price rises or falls” Tim Lawless, head of research, CoreLogic

“Lifestyles will undoubtedly change, which will make living outside the inner city more appealing. If you don’t have to go to the CBD every day for work, because you can work from home, then you don’t have to live near it.”

How this will impact the spring selling season, which is traditionally the busiest season for property markets, is unpredictable.

Andrew Bartolo, ME general manager home loans, says the property market “notoriously blooms in spring” with a flurry of listings and buyers preparing to pounce.

Andrew Bartolo, general manager home loans, ME

Andrew Bartolo, general manager home loans, ME

“But this season will be different: the property market will be quieter due to the impact of COVID-19, particularly in Melbourne. Despite some more listings this spring and record-low interest rates, economic concerns will dampen demand,” he says.

“Plenty of challenges remain, including high levels of unemployment, job insecurity and lower immigration, impacting people’s willingness to transact in property. Many Australians are also on home loan repayment pauses, and the gradual end of this type of support will be a critical juncture for the property market going forward.”

In terms of demand, buyer activity is expected to be lower overall than in previous spring buying seasons, Bartolo says, although buyers are still there and have a strong appetite for potential bargain buys.

“ME has seen an influx of first home buyers and expects this to continue. Potential for price falls and reduced investor activity, together with historically low interest rates and government support, are propelling first home buyers into action,” he says.

“The fallout of the COVID-19 pandemic and lockdowns has caused a short supply of stock. However, this spring we may see an increase in listings come onto the market. I don’t foresee new stock overwhelming current demand, but certainly anyone listing will be met with a high degree of enquiry.”

Bartolo backs up Koulizos’s sentiments that the pandemic may prompt a more wholesale shift in priorities when it comes to homebuying trends, with proximity to your place of employment no longer as important as it once was.

“COVID-19 has led to a reassessment of life priorities. According to ME’s latest Quarterly Property Sentiment Report, 45% of respondents said they were more likely to consider buying in a regional area to save money and improve their lifestyle − rising to 60% of first home buyers,” Bartolo explains.

“New remote and flexible working arrangements have made buying in regional areas a more feasible and affordable lifestyle option, and as such we may start seeing more buyers making their move this spring.”

https://www.brokernews.com.au/features/analysis/six-months-in-how-are-house-prices-faring-273734.aspx