Stamp duty

[et_pb_section][et_pb_row][et_pb_column type=”4_4″][et_pb_text]

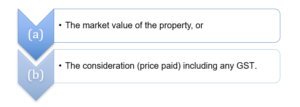

Stamp duty is imposed on most transfers of property unless exempt by statute. The duty payable is based on the greater of:

Stamp duty is payable according to a sliding scale that varies between jurisdictions. To determine the amount of stamp duty payable on a transfer of property, see the following example:

Example:

Table 11.1 Victorian stamp duty rates

| Property value | Duty payable |

| 0 – $25,000 | 1.4 % of the dutiable value of the property |

| $25,000 – $130,000 | $350 + 2.4% of the dutiable value in excess of $25,000 |

| $130,001-$960,000 | $2,870 plus 6% of the dutiable value in excess of $130,000 |

| More than $960,000 | 5.5% of the dutiable value |

If you don’t pay your duty within 30 days of settlement, penalty tax and interest may apply.

**reference http://www.sro.vic.gov.au/node/1491 (29/6/2016)

How does stamp duty in Victoria compare with other States?

Refer to Appendix 1, Table 11: Stamp duty websites

Table 11.2: Stamp duty rates by State

| Purchase price | $1 million | $500,000 | $250,000 |

| Victoria | 55,000 | 25,070 | 10,070 |

| South Australia | 48,830 | 21,330 | 8,955 |

| Western Australia | 42,616 | 17,765 | 6,935 |

| NSW | 40,490 | 17,990 | 7,240 |

| Tasmania | 40,185 | 18,248 | 7,935 |

| Queensland | 30,850 | 8,750 | 2,500 |

Stamp duty concessions are available where the purchaser is a first home buyer.

Each State and Territory Revenue Office is responsible for administering the collection of stamp duty and any concessions for first home buyers Table 5.2 illustrates that there are differences between the States. Further differences include the imposition of duty on mortgages and charges except in Victoria. Only New South Wales and Queensland impose duty on the grant of lease of real property. Thus stamp duty costs will vary from State to State on different transactions.

Shares in a business considered to be a land-rich corporation are also subject to stamp duty. In Victoria ‘land rich’ provisions are triggered if the following elements are present:

If the ‘land rich’ provisions are satisfied, stamp duty is charged on the land transfer rates rather than the share transfer rates. If a stamp duty assessment is not paid, the tax commissioner has the right to put a charge over the property. Bodies that provide or promote outdoor sporting activities

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]