How many years does it take a WA uni graduate to pay off their HECS debt? The figure is rising

May 2022Karen Millers

Categories

Location ReportsMedia releasesNational market updatesPersonal advisersPIPA AdviserPIPA Annual Investor Sentiment SurveysPIPA Member ProfilesPIPA video updatesPIPA webinarsPodcastsProperty advisersProperty newsLatest Articles

Rent rises ease but crisis’ link to population density found to be tenuous

Jordan van den Berg: The ‘Robin Hood’ TikToker taking on Australian landlords

Victorian property investors face yet another new property tax as council tests levy

Rentvesting in Australia: A deep dive

‘More chance of winning lotto’ than housing targets being met

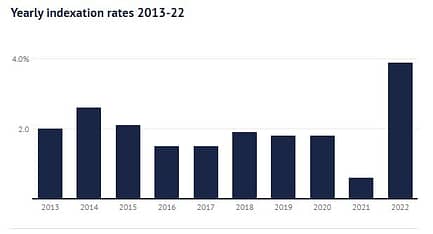

Rising inflation will see university debt loans increase by 3.9 per cent on June 1 with many already struggling to repay their loan.

The Higher Education Loan Program, formerly HECS, is a government loan to help cover university fees. Students only begin to repay the loan when they start to earn more than a threshold currently set at $47,014.

These payments are a percentage of their annual earnings that increases as their income does from a rate of 1 per cent up to 10 per cent.

The Australian Taxation Office, which administers student loan repayments, this month set the CPI indexation rate that will be applied to all student loans on June 1 at 3.9 per cent.

That means anyone with a student loan who earns between $47,014 and up to $70,000 is likely to see their loan increase, despite paying the minimum repayment rate.

It’s a steep increase from 2021, when the indexation rate was just 0.6 per cent and the preceding five years, which were all indexed at less than 2 per cent.

Rocky McGellin, 29, currently owes $50,000 for his Bachelor of Arts and Masters of Science Communications.

“At my current repayment rate of about $3000 a year, or $110 each pay, it’ll be about 18 years before it’s paid off in full and that’s not including indexation,” he said.

“Some people say a student loan is the best debt you can get, but it’s also one of the hardest to pay off because it’s there quietly nibbling away at your paycheck each fortnight.

“With wages stagnating and the CPI indexation increasing, how am I ever supposed to pay it off in full?”

Data released on Wednesday showed wages grew just 0.7 per cent in the three months to the end of March and 2.4 per cent for the year — well below annual inflation of 5.1 per cent.

In WA, wages grew just 2.2 per cent for the year and 0.5 per cent in the quarter.

Meanwhile university fees in Australia have skyrocketed in the past 30 years, and now sit at an all-time high.

Significant changes to university funding in 2020 saw the government increase student contribution amounts towards degrees such as law and communications, and decreased it for others such as nursing, in an attempt to entice students into areas where more graduates were needed.

An undergraduate bachelor degree can cost $20,000-$45,000 with the cost of some courses such as veterinary science and medicine much higher.

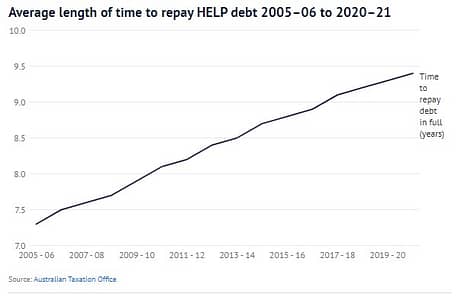

Data from the Australian Tax Office shows the time taken to repay student debts has been rising, reaching an average of 9.4 years in 2020–21, more than a year longer than it was a decade ago when the average HELP balance was $15,191.

If the Greens hold the balance of power in the Senate one of their key measures will be to wipe student debt and abolish university fees.

WA Greens Senator Dorinda Cox said 2.9 million people owed an average of $23,685 in study debt in 2020-21.

“Many current MPs, including the Prime Minister, went to university when it was free,” she said.

“With the cost of living and housing prices skyrocketing, abolishing student debt is a cheaper and fairer way of tackling cost of living pressures.”

Cox said to wipe all student debt would cost $33 billion over the forward estimates and $60.7 billion over the decade, about a third of the $184 billion cost of the stage 3 tax cuts.

“Analysis prepared by the Parliamentary Budget Office finds that in 2024-25, the benefit of the government’s proposed tax cuts will overwhelmingly flow to higher income earners and men, while the benefit of the Greens’ plan to wipe student debt will flow to low and middle income earners and women,” she said.

Property Investment Professionals of Australia chair Nicola McDougall said women were disproportionately impacted by mounting student debts.

“A way to ease the [HELP] burden on women would be to apply an inflation freeze during any periods of maternity leave or when they are out of the workforce so that their university debts are not skyrocketing,” she said.

“That way, when they do return to work, they are not faced with a debt that has ballooned significantly, just because they took time out to care for their children.”

McDougall said compulsory repayment of university debt was one of the reasons women decided to leave the workforce to care for children.

“Essentially, with childcare costs and tax considerations, if they continued to work part-time they may be left with no take-home pay at all, so it makes little financial sense at the time,” she said.

Independent economist Saul Eslake said applying a freeze while women were on maternity leave was a sensible idea, but questioned the efficacy of wiping all student loans.

“Wiping student debt would help women who typically earn less than men and are more likely to spend time out of the workforce caring for children or elderly relatives,” he said.

“It would help those ex-students on lower incomes – but it would also help students who have gone on to earn high salaries soon after graduating, such as lawyers and investment bankers, and I would question why they should be assisted in that way.

“A better policy would be to erase or reduce student debt for ex-students whose income falls below some threshold, with a phase-out for people on incomes above that threshold.”

Sarah Brookes, Sydney Morning Herald, 19 May 2022

https://www.smh.com.au/national/western-australia/how-many-years-does-it-take-a-wa-uni-graduate-to-pay-off-their-hecs-debt-the-figure-is-rising-20220518-p5amf5.html